I’ve said this before, and I’ll say it again: I’m not an economist. While I certainly look to the experts for information, more often than not I base my opinions on my own “empirical” experiences, i.e., what I observe. For purposes of this article, what I’ve been reading about and experiencing for myself, is the trend in home improvement spending. Now, we all know that home improvement spending has hit record highs over the last eighteen months; up in 2021 by 28% from 2020. The question is, will the gains in household spending continue, especially given the inflationary rise in household furnishings prices we’ve seen lately.

According to CNBC in their February 10 article, “Here is how Inflation is Hitting Everything You Buy for Your Home”:

- Floor coverings: 0.8% month over month, 7.2% year over year

- Window coverings: 1.8% month over month, 16.2% year over year

- Furniture/bedding: 2.4% month over month, 17% year over year

- Bedroom furniture: 1.8% month over month, 13.7% year over year

- Clocks, lamps and decorator items: 2.7% month over month, 6.3% year over year

- Living room/kitchen/dining room furniture: 2.2% month over month, 19.9% year over year

- Appliances: 1.5% month over month, 8.5% year over year

Sure, prices on home furnishings have gone up. But does that mean that folks are done spending on their homes? I don’t think so. The article goes onto say that “People tend to upgrade home furnishings after they remodel” and we’re just now on the tail end of the greatest home remodeling era in history. To me, and this is proven out I believe by the foot traffic in home furnishings stores, we are now in a “post remodeling” home furnishings boom.

In late November of last year, Furniture Today made this prediction in an article entitled Spruce-up Splurge: “A new coat of paint, the addition of a piece of accent furniture, some updated wall art — it all adds up to become part of a larger redecorating budget for consumers, many of whom plan to spend between $2,000 and $4,999 on their home décor in a year’s time. Our study found that 26% of all respondents — with little variation by age group — plan to spend that amount over a 12-month period beginning in mid-2021. Another nearly 40% expected to commit between $500 and $1,999, again, fairly evenly distributed by generation. Meanwhile, at 11%, Baby Boomers are the most likely to ante $10,000 or more when sprucing up their homes.”

Building material retailers, furniture and home décor retailers, security system dealers… there’s a tremendous amount of money changing hands here. And while the hands accepting the cash represent a wide variety of service and product providers, they all have one thing in common: It's really not “cash” that’s exchanging hands here. It’s credit.

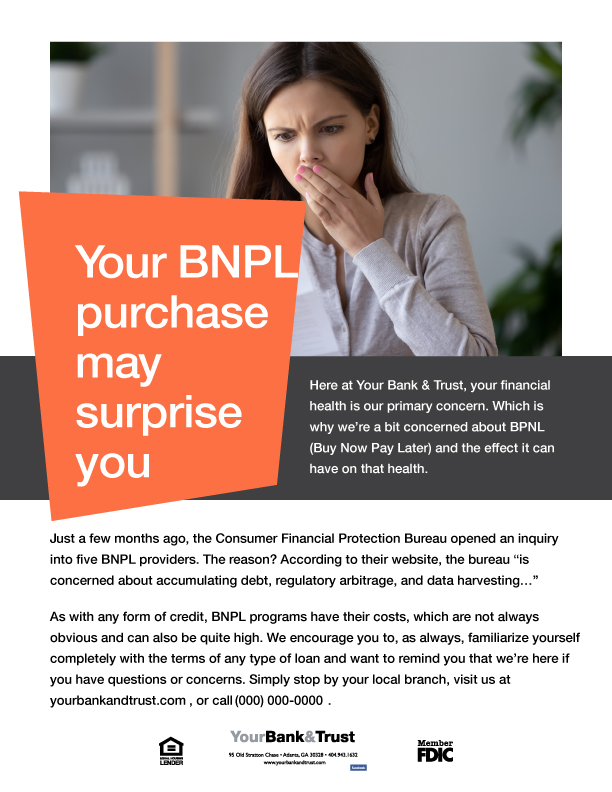

The home furnishings store aisles are crowded not just with shoppers, but messaging around buy now, pay later programs. Go into any home décor store and you’ll see signs down every aisle, encouraging shoppers to make a purchase now (regardless of whether they can truly afford to or not) and not worry about paying for it until later. The Buy Now Pay Later (BNPL) industry is booming, having generated nearly $100 billion in 2020, and projected to reach $3.98 trillion by 2030.

What does this mean for community banks? Here at BankMarketingCenter.com, we believe that this is an opportunity for banks to build their business by offering their customers alternative financing… financing that would, for instance, help improve their credit score. That’s because, unbeknownst to many BNPL borrowers, these point-of-sale loans do not routinely appear on most credit reports. That means a good payment record on your buy now, pay later account won't help you build credit. Another “favor” you’re doing your customers? The Financial Brand points out that “16% of users admit to having had regrets over BNPL purchases. Among the reasons: the purchase was ultimately too expensive; late fees were high; easy credit led to buying something not needed; and finding that some lenders’ policy  of not putting BNPL deals through credit bureaus meant the debt did not build credit.”

of not putting BNPL deals through credit bureaus meant the debt did not build credit.”

Why not take this opportunity to let your customers know that you offer the kind of financing that truly makes sense and meets their needs? Personal loans, for instance or better still, a HELOC, where they only pay interest on what they actually spend? If you’re a community bank and this appeals to you, the good news is that we’ve already created the messaging! All you need to do is visit our site to learn how you can easily customize it with your brand colors and logo, change the copy if you wish, and choose from the thousands of fee-free images we offer. You can do all of the above without any special software of any design skill whatsoever. Our financial industry marketing professionals have already done all of the work for you!

About Bank Marketing Center

Here at BankMarketingCenter.com, our goal is to help you with that topical, compelling communication with customers; the messaging — developed by banking industry marketing professionals, well trained in the thinking behind effective marketing communication — that will help you build trust, relationships, and revenue. In short, build your brand. To view our campaigns, both print and digital, visit BankMarketingCenter.com. Or, you can contact me directly by phone at 678-528-6688 or email at nreynolds@bankmarketingcenter.com.